| Part of a series on |

| Taxation |

|---|

|

| An aspect of fiscal policy |

Tax evasion is an illegal attempt to defeat the imposition of taxes by individuals, corporations, trusts, and others. Tax evasion often entails the deliberate misrepresentation of the taxpayer's affairs to the tax authorities to reduce the taxpayer's tax liability, and it includes dishonest tax reporting, declaring less income, profits or gains than the amounts actually earned, overstating deductions, using bribes against authorities in countries with high corruption rates and hiding money in secret locations.

Tax evasion is an activity commonly associated with the informal economy.[1] One measure of the extent of tax evasion (the "tax gap") is the amount of unreported income, which is the difference between the amount of income that the tax authority requests be reported and the actual amount reported.

In contrast, tax avoidance is the legal use of tax laws to reduce one's tax burden. Both tax evasion and tax avoidance can be viewed as forms of tax noncompliance, as they describe a range of activities that intend to subvert a state's tax system, but such classification of tax avoidance is disputable since avoidance is lawful in self-creating systems.[2] Both tax evasion and tax avoidance can be practiced by corporations, trusts, or individuals.

YouTube Encyclopedic

-

1/5Views:25 88225 0122 014 536108 824574

-

What is Tax Evasion?

-

Shakira Tax Haven Strategy Explained (she only paid 2% tax)

-

Selling a Lamborghini To Pay Off Tax Evasion 😵 💫

-

Tax Evasion using ₹40 Crore Building | Income Tax Case Study

-

What is Tax Evasion | Government Penalties on Tax Evasion | Methods of Tax Evasion

Transcription

Economics

In 1968, Nobel laureate economist Gary Becker first theorized the economics of crime,[4] on the basis of which authors M.G. Allingham and A. Sandmo produced, in 1972, an economic model of tax evasion. This model deals with the evasion of income tax, the main source of tax revenue in developed countries. According to the authors, the level of evasion of income tax depends on the detection probability and the level of punishment provided by law.[5] Later studies, however, pointed limitations of the model, highlighting that individuals are also more likely to comply with taxes when they believe that tax money is appropriately used and when they can take part on public decisions.[6][7][8][9]

The literature's theoretical models are elegant in their effort to identify the variables likely to affect non-compliance. Alternative specifications, however, yield conflicting results concerning both the signs and magnitudes of variables believed to affect tax evasion. Empirical work is required to resolve the theoretical ambiguities. Income tax evasion appears to be positively influenced by the tax rate, the unemployment rate, the level of income and dissatisfaction with government.[10] The U.S. Tax Reform Act of 1986 appears to have reduced tax evasion in the United States.[11]

In a 2017 study Alstadsæter et al. concluded based on random stratified audits and leaked data that occurrence of tax evasion rises sharply as amount of wealth rises and that the very richest are about 10 times more likely than average people to engage in tax evasion.[12]

Tax gap

The tax gap describes how much tax should have been raised in relation to much tax is actually raised. The IRS defines the gross tax gap as the difference between the true tax liability for a given year and the taxes actually remitted on time. It comprises the nonfiling gap, the underreporting gap, and the underpayment (or remittance) gap. Voluntary tax compliance in the U.S. is approximately 85% of taxes actually due, leaving a gross tax gap of about 15%.

The tax gap is growing mainly because of two factors, the lack of enforcement on the one hand and the lack of compliance on the other hand. The former is mainly rooted in the costly enforcement of the taxation law.[14] The latter is based on the foundation that tax compliance is costly for individuals as well as firms (tax filling, bureaucracy), hence not paying taxes would be more economical in their opinion.

Evasion of customs duty

Customs duties are an important source of revenue in developing countries.[citation needed][clarification needed] Importers attempt to evade customs duty by (a) under-invoicing and (b) misdeclaration of quantity and product-description. When there is ad valorem import duty, the tax base can be reduced through under-invoicing. Misdeclaration of quantity is more relevant for products with specific duty. Production description is changed to match a H. S. Code commensurate with a lower rate of duty.[15][better source needed]

Smuggling

Smuggling is import or export of products by illegal means.[citation needed] Smuggling is resorted to for total evasion of customs duties, as well as for the import and export of contraband. Smugglers do not pay duty since the transport is covert, so no customs declaration is made.[15][better source needed]

Evasion of value-added tax and sales taxes

During the second half of the 20th century, value-added tax (VAT) emerged as a modern form of consumption tax throughout the world, with the notable exception of the United States. Producers who collect VAT from consumers may evade tax by under-reporting the amount of sales.[17] The US has no broad-based consumption tax at the federal level, and no state currently collects VAT; the overwhelming majority of states instead collect sales taxes. Canada uses both a VAT at the federal level (the Goods and Services Tax) and sales taxes at the provincial level; some provinces have a single tax combining both forms.[citation needed]

In addition, most jurisdictions which levy a VAT or sales tax also legally require their residents to report and pay the tax on items purchased in another jurisdiction.[citation needed] This means that consumers who purchase something in a lower-taxed or untaxed jurisdiction with the intention of avoiding VAT or sales tax in their home jurisdiction are technically breaking the law in most cases.

This is especially prevalent in federal countries like the United States and Canada where sub-national jurisdictions charge varying rates of VAT or sales tax.

In liberal democracies, a fundamental problem with inhibiting evasion of local sales taxes is that liberal democracies, by their very nature, have few (if any) border controls between their internal jurisdictions. Therefore, it is not generally cost-effective to enforce tax collection on low-value goods carried in private vehicles from one jurisdiction to another with a different tax rate. However, sub-national governments will normally seek to collect sales tax on high-value items such as cars.[18]

Objectives to evade taxes

One reason for taxpayers to evade taxes is the personal benefits that come with it, thus the individual problems that lead to that decision[19] Additionally, Wallschutzky's exchange relationship hypothesis[20][21] presents as a sufficient motive for many. The exchange relationship hypothesis states that tax payers believe that the exchange between their taxes and the public good/social services as unbalanced.[22] Furthermore, the little capability of the system to catch the tax evaders reduces associated risk.[citation needed] Most often, it is more economical to evade taxes, being caught and paying a fine as a consequence, than paying the accumulated tax burden over the years.[citation needed] Thus, evasion numbers should be even higher than they are, hence for many people there seem to be moral objective countering this practice.[citation needed]

Government response

The level of evasion depends on a number of factors, including the amount of money a person or a corporation possesses. Efforts to evade income tax decline when the amounts involved are lower.[citation needed] The level of evasion also depends on the efficiency of the tax administration. Corruption by tax officials makes it difficult to control evasion. Tax administrations use various means to reduce evasion and increase the level of enforcement: for example, privatization of tax enforcement[15] or tax farming.[23][24]

In 2011 HMRC, the UK tax collection agency stated that it would continue to crack down on tax evasion, with the goal of collecting £18 billion in revenue before 2015.[citation needed] In 2010, HMRC began a voluntary amnesty program that targeted middle-class professionals and raised £500 million.[25]

Corruption by tax officials

Corrupt tax officials co-operate with the taxpayers who intend to evade taxes. When they detect an instance of evasion, they refrain from reporting it in return for bribes. Corruption by tax officials is a serious problem for the tax administration in many[which?] countries.[citation needed]

Level of evasion and punishment

Tax evasion is a crime in almost all developed countries, and the guilty party is liable to fines and/or imprisonment. In Switzerland, many acts that would amount to criminal tax evasion in other countries are treated as civil matters. Dishonestly misreporting income in a tax return is not necessarily considered a crime. Such matters are handled in the Swiss tax courts, not the criminal courts.[citation needed]

In Switzerland, however, some tax misconduct (such as the deliberate falsification of records) is criminal. Moreover, civil tax transgressions may give rise to penalties. It is often considered that the extent of evasion depends on the severity of punishment for evasion.

Privatization of tax enforcement

Professor Christopher Hood first[citation needed] suggested privatization of tax enforcement to control tax evasion more efficiently than a government department would,[26] and some governments have adopted this approach. In Bangladesh, customs administration was partly privatized in 1991.[15][better source needed]

Abuse by private tax collectors (see tax farming below) has on occasion led to revolutionary overthrow of governments who have outsourced tax administration.

Tax farming

Tax farming is an historical means of collection of revenue. Governments received a lump sum in advance from a private entity, which then collects and retains the revenue and bears the risk of evasion by the taxpayers. It has been suggested that tax farming may reduce tax evasion in less developed countries.[23]

This system may be liable to abuse by the "tax-farmers" seeking to make a profit, if they are not subject to political constraints. Abuses by tax farmers (together with a tax system that exempted the aristocracy) were a primary reason for the French Revolution that toppled Louis XVI.[citation needed]

PSI agencies

Pre-shipment inspection agencies like Société Générale De Surveillance S. A. and its subsidiary Cotecna are in business to prevent evasion of customs duty through under-invoicing and misdeclaration.

However, PSI agencies have cooperated with importers in evading customs duties. Bangladeshi authorities found Cotecna guilty of complicity with importers for evasion of customs duties on a huge scale.[27] In August 2005, Bangladesh had hired four PSI companies – Cotecna Inspection SA, SGS (Bangladesh) Limited, Bureau Veritas BIVAC (Bangladesh) Limited and INtertek Testing Limited – for three years to certify price, quality and quantity of imported goods. In March 2008, the Bangladeshi National Board of Revenue cancelled Cotecna's certificate for serious irregularities, while importers' complaints about the other three PSI companies mounted. Bangladesh planned to have its customs department train its officials in "WTO valuation, trade policy, ASYCUDA system, risk management" to take over the inspections.[28]

Cotecna was also found to have bribed Pakistan's prime minister Benazir Bhutto to secure a PSI contract by Pakistani importers. She and her husband were sentenced both in Pakistan and Switzerland.[29]

By continent

Asia

India

United Arab Emirates

In early October 2021, 11.9 million leaked financial records in addition to 2.9 TB of data was released in the name of Pandora Papers by the International Consortium of Investigative Journalists (ICIJ), exposing the secret offshore accounts of around 35 world leaders in tax havens to evade taxes. One of the many leaders to be exposed was the ruler of Dubai and prime minister of the United Arab Emirates, Sheikh Mohammed bin Rashid al-Maktoum. Sheikh Mohammed was identified as the shareholder of three firms that were registered in the tax havens of Bahamas and British Virgin Islands through an Emirati company, partially owned by an investment conglomerate, Dubai Holding and Axiom Limited, major shares of which were owned by the ruler.[33]

As per the leaked records, the Dubai ruler owned a massive number of upmarket and luxurious real estate across Europe via the cited offshore entities registered in tax havens.[34]

Additionally, the Pandora Papers also cites that the former Managing Director of IMF and French finance minister, Dominique Strauss-Kahn was permitted to create a consulting firm in the United Arab Emirates in 2018 after the expiry of tax exemptions of his Moroccan company, which he used for receiving millions of dollars worth of tax free consulting fees.[35]

Europe

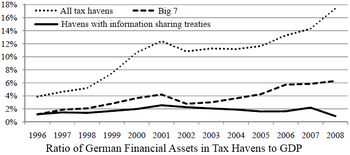

Germany, France, Italy, Denmark, Belgium

A network of banks, stock traders and top lawyers has obtained billions from the European treasuries through suspected fraud and speculation with dividend tax. The five hardest hit countries have lost together at least $62.9 billion.[36] Germany is the hardest hit country, with around €31 billion withdrawn from the German treasury.[37] Estimated losses for other countries include at least €17 billion for France, €4.5 billion in Italy, €1.7 billion in Denmark and €201 million for Belgium.[38][39][40]

Greece

A paper by economists Annette Alstadsæter, Niels Johannesen and Gabriel Zucman, which used data from HSBC Switzerland ("Swiss leaks") and Mossack Fonseca ("Panama Papers"), found that "on average about 3% of personal taxes are evaded in Scandinavia, but this figure rises to about 30% in the top 0.01% of the wealth distribution... Taking tax evasion into account increases the rise in inequality seen in tax data since the 1970s markedly, highlighting the need to move beyond tax data to capture income and wealth at the top, even in countries where tax compliance is generally high. We also find that after reducing tax evasion—by using tax amnesties—tax evaders do not legally avoid taxes more. This result suggests that fighting tax evasion can be an effective way to collect more tax revenue from the ultra-wealthy."[41]

United Kingdom

HMRC, the UK tax collection agency, estimated that in the tax year 2016–17, pure tax evasion (i.e. not including things like hidden economy or criminal activity) cost the government £5.3 billion. This compared to a wider tax gap (the difference between the amount of tax that should, in theory, be collected by HMRC, against what is actually collected) of £33 billion in the same year, an amount that represented 5.7% of liabilities. At the same time, tax avoidance was estimated at £1.7 billion (this does not include international tax arrangements that cannot be challenged under the UK law, including some forms of base erosion and profit shifting (BEPS)).[42]

In 2013, the Coalition government announced a crackdown on economic crime. It created a new criminal offence for aiding tax evasion and removed the requirement for tax investigation authorities to prove "intent to evade tax" to prosecute offenders.[43]

In 2015, Chancellor of the Exchequer George Osborne promised to collect £5 billion by "waging war" on tax evaders by announcing new powers for HMRC to target people with offshore bank accounts.[44] The number of people prosecuted for tax evasion doubled in 2014/15 from the year before to 1,258.[45]

United States

In the United States of America, Federal tax evasion is defined as the purposeful, illegal attempt to evade the assessment or the payment of a tax imposed by federal law. Conviction of tax evasion may result in fines and imprisonment.[46]

The Internal Revenue Service (IRS) has identified small businesses and sole proprietors as the largest contributors to the tax gap between what Americans owe in federal taxes and what the federal government receives. Small businesses and sole proprietorships contribute to the tax gap because there are few ways for the government to know about skimming or non-reporting of income without mounting significant investigations.

As of 2007[update] the most common means of tax evasion was overstatement of charitable contributions, particularly church donations.[47]

Estimates of lost government revenue

The IRS estimates that the 2001 tax gap was $345 billion and for 2006 it was $450 billion.[48] A study of the 2008 tax gap found a range of $450–$500 billion, and unreported income to be about $2 trillion, concluding that 18 to 19 percent of total reportable income was not being properly reported to the IRS.[10]

Tax evasion and inequality

Generally, individuals tend to evade taxes, while companies rather avoid taxes. There is a great heterogenic among people who evade people as it is a substantial issue in society, that is creating an excessive tax gap. Studies suggest that 8% of global financial wealth lies in offshore accounts.[49] Often, offshore wealth that is stored in tax havens stays undetected in random audits.[50] Even though there is high diversity among people who evade taxes, there is a higher probability among the highest wealth group. According to Alstadsæter, Johannesen and Zucman 2019 the extent of taxes evaded is substantially higher with higher income, and exceptionally higher among people of the top wealth group.[49] In line with this, the probability to appear in the Panama Papers rises significantly among the top 0.01% of the wealth group, as does the probability to own an unreported account at HSBC. However, the upper wealth group is also more inclined to use tax amnesty.[49]

See also

- Fuel dyes

- Global Forum on Transparency and Exchange of Information for Tax Purposes

- History of tax resistance

- Informal sector

- Land value tax

- Paradise Papers

- Social inequality

- Tax amnesty

- Tax information exchange agreements

- Tax noncompliance

- Tax resistance

- Taxation as slavery

- Taxation as theft

- Unreported employment

- U.S. taxation of illegal income

Further reading

- Slemrod, Joel. 2019. "Tax Compliance and Enforcement." Journal of Economic Literature, 57 (4): 904–54.

- Emmanuel Saez and Gabriel Zucman. 2019. The Triumph of Injustice: How the Rich Dodge Taxes and How to Make Them Pay. W.W. Norton.

References

- ^ Tax Evasion & Whistleblowers: Curious Policy or Durable Strategy? Tax Law: International & Comparative Tax eJournal. SSRN. Accessed 5 May 2020.

- ^ Michael Wenzel (2002). "The Impact of Outcome Orientation and Justice Concerns on Tax Compliance" (PDF). Journal of Applied Psychology: 4–5.

When taxpayers try to find loopholes with the intention to pay less tax, even if technically legal, their actions may be against the spirit of the law and in this sense considered noncompliant.

{{cite journal}}: Cite journal requires|journal=(help) - ^ Hebous, Shafik (2011). "Money at the Docks of Tax Havens: A Guide" (PDF). CESifo Working Paper Series. 70 (3587): 9. doi:10.1628/001522114X684547. hdl:10419/52472. S2CID 39873207. SSRN 1934164.

- ^ Gary Becker (1968). "Crime and Punishment: An Economic Approach" (PDF). The Journal of Political Economy. 76 (2): 169–217. doi:10.1086/259394.

- ^ Allingham, M. G. and A. Sandmo [1972] 'Income Tax evasion: A Theoretical Analysis', Journal of Public Economics, Vol. 1, 1972, pp. 323–38.

- ^ Torgler, Benno (2007-01-01). Tax Compliance and Tax Morale: A Theoretical and Empirical Analysis. Edward Elgar Publishing. ISBN 978-1-84720-720-3.

- ^ Touchton, Michael; Wampler, Brian; Peixoto, Tiago (2021). "Of democratic governance and revenue: Participatory institutions and tax generation in Brazil". Governance. 34 (4): 1193–1212. doi:10.1111/gove.12552. ISSN 1468-0491. S2CID 228863220.

- ^ Alm, James (2012-02-01). "Measuring, explaining, and controlling tax evasion: lessons from theory, experiments, and field studies". International Tax and Public Finance. 19 (1): 54–77. doi:10.1007/s10797-011-9171-2. ISSN 1573-6970. S2CID 8221198.

- ^ Torgler, Benno (2005-06-01). "Tax morale and direct democracy". European Journal of Political Economy. 21 (2): 525–531. doi:10.1016/j.ejpoleco.2004.08.002. ISSN 0176-2680.

- ^ a b Cebula, Richard; Feige, Edgar L. (n.d.). "America's Underground Economy: Measuring the Size, Growth and Determinants of Income Tax Evasion in the U.S". Mpra Paper. Ideas.repec.org.

- ^ Kinsey, Karyl A.; Grasmick, Harold G. (1993). "Did the Tax Reform Act of 1986 Improve Compliance? Three Studies of Pre- and Post-TRA Compliance Attitudes*". Law & Policy. 15 (4): 293–325. doi:10.1111/j.1467-9930.1993.tb00111.x. ISSN 1467-9930.

- ^ Alstadsæter et al. 2017. Tax Evasion and Inequality∗

- ^ Lopez, German; Wu, Ashley (August 26, 2022). "Conspiracy Theories / How more funding for the I.R.S. became a political firestorm". The New York Times. Archived from the original on August 26, 2022.

Source: U.S. Department of Treasury; Estimates from 2019

- ^ Sandmo, Agnar (2005). "The Theory of Tax Evasion: A Retrospective View". National Tax Journal. 58 (4): 643–663. doi:10.17310/ntj.2005.4.02. hdl:11250/162784. S2CID 4847820 – via JSTOR.

- ^ a b c d Chowdhury, F. L. (1992) Evasion of Customs Duty in Bangladesh, unpublished MBA dissertation, Graduate School of Management, Monash University, Australia.[better source needed]

- ^ David Cay Johnston (13 December 2011). "Where's the fraud, Mr. President?". Reuters. Archived from the original on 7 January 2012.

- ^ Spiro, Peter S. (2005), "Tax Policy and the Underground Economy," in Christopher Bajada and Friedrich Schneider, eds., Size, Causes and Consequences of the Underground Economy (Ashgate Publishing).

- ^ Tomášková, Eva (2008). "Tax Evasion in the Czech Republic – In: A Brief Introduction to Czech Law. Rincon: The American Institute for Central European Legal Studies (AICELS) 2008. pp. 111–21 ISBN 978-0-692-00045-8" (PDF). Archived from the original (PDF) on September 3, 2011.

- ^ Allingham, Michael G.; Sandmo, Agnar (1972-11-01). "Income tax evasion: a theoretical analysis". Journal of Public Economics. 1 (3–4): 323–338. doi:10.1016/0047-2727(72)90010-2. ISSN 0047-2727.

- ^ Wallschutzky, Ian G. (1988). The effects of tax reform on tax evasion. Sydney: Australian Tax Research Foundation. ISBN 0-949482-23-4. OCLC 20053454.

- ^ Wallschutzky, I.G. (1984-12-01). "Possible causes of tax evasion". Journal of Economic Psychology. 5 (4): 371–384. doi:10.1016/0167-4870(84)90034-5. ISSN 0167-4870.

- ^ Cowell, F.A. (December 1992). "Tax evasion and inequity". Journal of Economic Psychology. 13 (4): 521–543. doi:10.1016/0167-4870(92)90010-5. ISSN 0167-4870.

- ^ a b Stella, Peter (1993). "Tax Farming: A Radical Solution for Developing Country Tax Problems?". IMF Staff Papers. 40 (1): 217–25. doi:10.2307/3867383. JSTOR 3867383. S2CID 153924531.

- ^ Alam. D (1999) Introduction of PSI system in Bangladesh: Facts and Documents, Desh Prokashon, Dhaka.

- ^ Russell, Jonathan (June 10, 2011). "HMRC opens 16 criminal cases over tax evasion". The Telegraph. London: telegraph.co.uk. Archived from the original on 2022-01-12. Retrieved August 12, 2011.

- ^ Hood, C. (1986) Privatizing UK tax Law Enforcement?, Public Administration, Vol. 64, Autumn, 1986, p. 319–33.

- ^ "NBR showcauses Cotecna on car import scam". New Age. Dhaka: Media New Age Ltd. 14 September 2007. Archived from the original on November 20, 2010.

- ^ "PSI system likely to continue". Bangladesh News. 3 May 2008. Archived from the original on May 11, 2008. Retrieved 3 January 2015.

- ^ Langley, Alison (6 August 2003). "Pakistan: Bhutto Sentenced In Switzerland". New York Times.

- ^ a b c Piketty, Thomas; Qian, Nancy (2015). "Income Inequality and Progressive Income Taxation in China and India, 1986–2015". American Economic Journal: Applied Economics. 1 (2): 53–63. doi:10.1257/app.1.2.53. S2CID 27331525.

- ^ In re 116 taxman.com 878 (AAR - New Delhi)

- ^ "Advance ruling applications for determining chargeability to capital gains tax under India-Mauritius tax treaty not admitted based on facts" (PDF). Retrieved 21 June 2023.

- ^ "World Leaders, Including Jordan's Abdullah, UAE's Sheikh Mohammed Found in Pandora Papers". The Media Line. 4 October 2021. Retrieved 4 October 2021.

- ^ "Pandora Papers: The offshore companies of UAE's Sheikh Mohammed". Middle East Eye. Retrieved 4 October 2021.

- ^ "Meet the European leaders named in the Pandora Papers". Politico. 4 October 2021. Retrieved 4 October 2021.

- ^ "CORRECTIV - Investigative. Independent. Non-profit". cumex-files.com. 18 October 2018. Archived from the original on 2018-10-18. Retrieved 2018-11-09.

- ^ Hill, Jenny (2017-06-09). "Germany fears huge losses in massive tax scandal". BBC News. Retrieved 2018-11-09.

- ^ "Kuppet mod Europa". DR (in Danish). Retrieved 2018-11-09.

- ^ Vartdal, Ragnhild. "Norge rammet av europeisk skatteskandale" [Norway affected by European tax scandal]. NRK (in Norwegian Bokmål). Retrieved 2018-11-09.

- ^ magazine, Le Point (2018-10-18). ""CumEx Files " : la fraude fiscale à 55 milliards d'euros" ["CumEx Files": tax fraud at 55 billion euros]. Le Point (in French). Retrieved 2018-11-09.

- ^ Alstadsæter, Annette; Johannesen, Niels; Zucman, Gabriel (23 October 2018). "Tax Evasion and Inequality" (PDF). gabriel-zucman.eu.

- ^ "Measuring tax gaps 2018 edition" (PDF). HM Revenue & Customs. 14 June 2018.

- ^ "UK government announces corporate tax evasion clampdown". BBC News. 19 March 2015.

- ^ "George Osborne wages war on tax evasion and avoidance". Channel 4 News. 19 March 2015.

- ^ Ames, Jonathan; Gibb, Frances (14 December 2015). "Lawyers and tradesmen caught in tax clampdown".

- ^ 26 U.S.C. § 7201.

- ^ Sabatini, Patricia (25 March 2007). "Tax Cheats Cost U.S. hundreds of billions". Pittsburgh Post-Gazette.

- ^ "Tax Gap for Tax Year 2006 Overview Jan. 6, 2012" (PDF). U.S. Internal Revenue Service. Retrieved 2012-06-14.

- ^ a b c Alstadsæter, Annette; Johannesen, Niels; Zucman, Gabriel (2019-06-01). "Tax Evasion and Inequality". American Economic Review. 109 (6): 2073–2103. doi:10.1257/aer.20172043. ISSN 0002-8282.

- ^ Guyton, John; Langetieg, Patrick; Reck, Daniel; Risch, Max; Zucman, Gabriel (2021-03-22). "Tax Evasion at the Top of the Income Distribution: Theory and Evidence". Working Paper Series. doi:10.3386/w28542. S2CID 233637494.

{{cite journal}}: Cite journal requires|journal=(help)

External links

- Tax Evasion and Fraud collected news and commentary at The Economist

- Tax Evasion collected news and commentary at The New York Times

- Employment Tax Evasion Schemes Archived 2017-06-29 at the Wayback Machine common employment schemes at IRS

- United States

- US Justice Dept press release on Jeffrey Chernick, UBS tax evader

- US Justice Tax Division and its enforcement efforts

Types of fraud | |

|---|---|

| Business-related | |

| Family-related | |

| Financial-related | |

| Government-related | |

| Other types | |

| National | |

|---|---|

| Other | |