![{\displaystyle \operatorname {E} [x]={\frac {{\sqrt {b}}\ K_{p+1}({\sqrt {ab}})}{{\sqrt {a}}\ K_{p}({\sqrt {ab}})}}}](https://wikimedia.org/api/rest_v1/media/math/render/svg/9eea374ea6d263f4dec6f737248ac6c7ee9edec4)

![{\displaystyle \operatorname {E} [x^{-1}]={\frac {{\sqrt {a}}\ K_{p+1}({\sqrt {ab}})}{{\sqrt {b}}\ K_{p}({\sqrt {ab}})}}-{\frac {2p}{b}}}](https://wikimedia.org/api/rest_v1/media/math/render/svg/4b8243064fe20b0eb33317bf58d29ad616bbd2ff)

![{\displaystyle \operatorname {E} [\ln x]=\ln {\frac {\sqrt {b}}{\sqrt {a}}}+{\frac {\partial }{\partial p}}\ln K_{p}({\sqrt {ab}})}](https://wikimedia.org/api/rest_v1/media/math/render/svg/f49d3a11593033dcb22f9bf4f12377957b4ecc5b)

![{\displaystyle \left({\frac {b}{a}}\right)\left[{\frac {K_{p+2}({\sqrt {ab}})}{K_{p}({\sqrt {ab}})}}-\left({\frac {K_{p+1}({\sqrt {ab}})}{K_{p}({\sqrt {ab}})}}\right)^{2}\right]}](https://wikimedia.org/api/rest_v1/media/math/render/svg/fb650b320e436e5cc35f33ed94c0794e9f4c58ea)

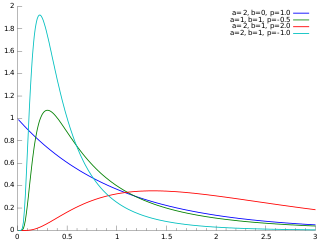

In probability theory and statistics, the generalized inverse Gaussian distribution (GIG) is a three-parameter family of continuous probability distributions with probability density function

where Kp is a modified Bessel function of the second kind, a > 0, b > 0 and p a real parameter. It is used extensively in geostatistics, statistical linguistics, finance, etc. This distribution was first proposed by Étienne Halphen.[1][2][3] It was rediscovered and popularised by Ole Barndorff-Nielsen, who called it the generalized inverse Gaussian distribution. Its statistical properties are discussed in Bent Jørgensen's lecture notes.[4]

YouTube Encyclopedic

-

1/5Views:14 793133 83584 7782 058666 260

-

Inverse Normal distribution: in the Natural Exponential Family

-

The Bell Curve (Normal/Gaussian Distribution) Explained in One Minute: From Definition to Examples

-

Understanding Generalized Linear Models (Logistic, Poisson, etc.)

-

GLM Link Function, and Canonical Links

-

Normal Distribution EXPLAINED with Examples

Transcription

Properties

Alternative parametrization

By setting and , we can alternatively express the GIG distribution as

where is the concentration parameter while is the scaling parameter.

Summation

Barndorff-Nielsen and Halgreen proved that the GIG distribution is infinitely divisible.[5]

Entropy

The entropy of the generalized inverse Gaussian distribution is given as[citation needed]

![{\displaystyle {\begin{aligned}H={\frac {1}{2}}\log \left({\frac {b}{a}}\right)&{}+\log \left(2K_{p}\left({\sqrt {ab}}\right)\right)-(p-1){\frac {\left[{\frac {d}{d\nu }}K_{\nu }\left({\sqrt {ab}}\right)\right]_{\nu =p}}{K_{p}\left({\sqrt {ab}}\right)}}\\&{}+{\frac {\sqrt {ab}}{2K_{p}\left({\sqrt {ab}}\right)}}\left(K_{p+1}\left({\sqrt {ab}}\right)+K_{p-1}\left({\sqrt {ab}}\right)\right)\end{aligned}}}](https://wikimedia.org/api/rest_v1/media/math/render/svg/4d663373bdf483797c0ce4ada0238439389242a3)

where is a derivative of the modified Bessel function of the second kind with respect to the order evaluated at

![{\displaystyle \left[{\frac {d}{d\nu }}K_{\nu }\left({\sqrt {ab}}\right)\right]_{\nu =p}}](https://wikimedia.org/api/rest_v1/media/math/render/svg/3838a857c40b56dee47ed55dade77403f6657cb8)

Characteristic Function

The characteristic of a random variable is given as(for a derivation of the characteristic function, see supplementary materials of [6] )

for where denotes the imaginary number.

Related distributions

Special cases

The inverse Gaussian and gamma distributions are special cases of the generalized inverse Gaussian distribution for p = −1/2 and b = 0, respectively.[7] Specifically, an inverse Gaussian distribution of the form

![{\displaystyle f(x;\mu ,\lambda )=\left[{\frac {\lambda }{2\pi x^{3}}}\right]^{1/2}\exp {\left({\frac {-\lambda (x-\mu )^{2}}{2\mu ^{2}x}}\right)}}](https://wikimedia.org/api/rest_v1/media/math/render/svg/430c36a80c0f4de08f8b56fe7019d79e5d8aea68)

is a GIG with , , and . A Gamma distribution of the form

is a GIG with , , and .

Other special cases include the inverse-gamma distribution, for a = 0.[7]

Conjugate prior for Gaussian

The GIG distribution is conjugate to the normal distribution when serving as the mixing distribution in a normal variance-mean mixture.[8][9] Let the prior distribution for some hidden variable, say , be GIG:

and let there be observed data points, , with normal likelihood function, conditioned on

where is the normal distribution, with mean and variance . Then the posterior for , given the data is also GIG:

where .[note 1]

Sichel distribution

The Sichel distribution[10][11] results when the GIG is used as the mixing distribution for the Poisson parameter .

Notes

- ^ Due to the conjugacy, these details can be derived without solving integrals, by noting that

- .

References

- ^ Seshadri, V. (1997). "Halphen's laws". In Kotz, S.; Read, C. B.; Banks, D. L. (eds.). Encyclopedia of Statistical Sciences, Update Volume 1. New York: Wiley. pp. 302–306.

- ^ Perreault, L.; Bobée, B.; Rasmussen, P. F. (1999). "Halphen Distribution System. I: Mathematical and Statistical Properties". Journal of Hydrologic Engineering. 4 (3): 189. doi:10.1061/(ASCE)1084-0699(1999)4:3(189).

- ^ Étienne Halphen was the grandson of the mathematician Georges Henri Halphen.

- ^ Jørgensen, Bent (1982). Statistical Properties of the Generalized Inverse Gaussian Distribution. Lecture Notes in Statistics. Vol. 9. New York–Berlin: Springer-Verlag. ISBN 0-387-90665-7. MR 0648107.

- ^ O. Barndorff-Nielsen and Christian Halgreen, Infinite Divisibility of the Hyperbolic and Generalized Inverse Gaussian Distributions, Zeitschrift für Wahrscheinlichkeitstheorie und verwandte Gebiete 1977

- ^ Pal, Subhadip; Gaskins, Jeremy (23 May 2022). "Modified Pólya-Gamma data augmentation for Bayesian analysis of directional data". Journal of Statistical Computation and Simulation. 92 (16): 3430–3451. doi:10.1080/00949655.2022.2067853. ISSN 0094-9655. S2CID 249022546.

- ^ a b Johnson, Norman L.; Kotz, Samuel; Balakrishnan, N. (1994), Continuous univariate distributions. Vol. 1, Wiley Series in Probability and Mathematical Statistics: Applied Probability and Statistics (2nd ed.), New York: John Wiley & Sons, pp. 284–285, ISBN 978-0-471-58495-7, MR 1299979

- ^ Dimitris Karlis, "An EM type algorithm for maximum likelihood estimation of the normal–inverse Gaussian distribution", Statistics & Probability Letters 57 (2002) 43–52.

- ^ Barndorf-Nielsen, O.E., 1997. Normal Inverse Gaussian Distributions and stochastic volatility modelling. Scand. J. Statist. 24, 1–13.

- ^ Sichel, Herbert S, 1975. "On a distribution law for word frequencies." Journal of the American Statistical Association 70.351a: 542-547.

- ^ Stein, Gillian Z., Walter Zucchini, and June M. Juritz, 1987. "Parameter estimation for the Sichel distribution and its multivariate extension." Journal of the American Statistical Association 82.399: 938-944.

See also